Andrew Yang warns American Dream odds have plummeted below 50 percent

The Statistical Decay of Upward Mobility

For decades, the American economic engine relied on a fundamental promise: work hard, and you will outpace your parents. Andrew Yang notes that for those born in the 1960s, this was nearly a mathematical certainty, with a 94% success rate. Today, that probability has plummeted. Data indicates that a child born now has a less than 50% chance of earning more than their predecessors. This inversion isn't just a number; it is a psychological wall that redefines how an entire generation views wealth and labor.

Higher Variance and the Lure of Aggressive Risk

When traditional paths—saving 10% of a salary or waiting for a 4% annual raise—no longer guarantee homeownership or stability, behavior shifts. Young people are increasingly adopting what Andrew Yang calls a higher variance strategy. If the middle-class dream feels statistically impossible, rolling the dice on volatile assets like Crypto or high-stakes sports betting feels like the only rational exit from mediocrity. This shift replaces prudent compounding with "all-or-nothing" gambles, often fueled by the distorted reality of social media success stories.

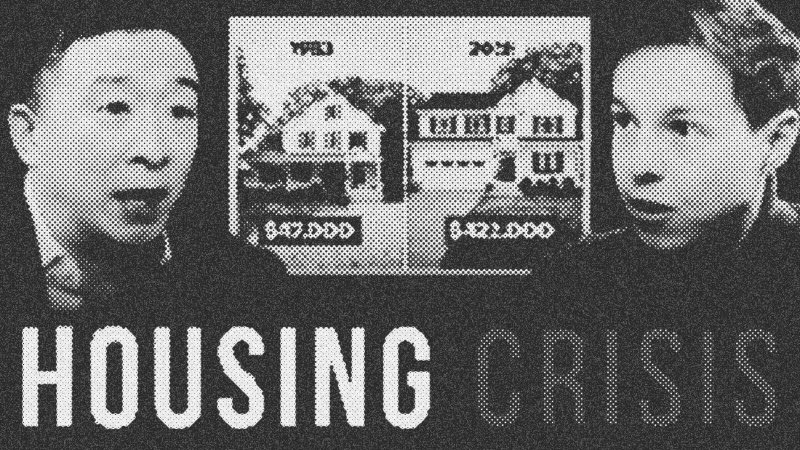

From Real Estate to Rolexes

As the average age of first-time homebuyers climbs toward 42, the markers of success have shifted from deeds to luxury goods. Many young adults are redirecting potential down payments toward Rolex or high-end vehicles. In their view, if a house is an unattainable $600,000 hurdle, a $15,000 watch provides a reachable, tangible signal of status. This pivot from long-term asset accumulation to immediate luxury consumption reflects a deeper resignation regarding the traditional financial timeline.

The Great Cultural Divide

Drawing on Nate Silver's framework in On the Edge, Andrew Yang describes a growing friction between the "River" and the "Village." The River people—entrepreneurs, investors, and risk-takers—operate in worlds of abundance and windfall. Conversely, the Village represents the stable but stagnant world of teachers and government workers. As the gap between these two groups widens, the social fabric strains, leaving those in the Village feeling the system is rigged while the River residents pursue trillion-dollar fortunes.

- Andrew Yang

- 21%· people

- Crypto

- 7%· products

- DraftKings

- 7%· products

- Elon Musk

- 7%· people

- ESPN

- 7%· companies

- Other topics

- 50%

Why It Feels IMPOSSIBLE to Get Rich Today | Andrew Yang

WatchThe Iced Coffee Hour Clips // 12:32

Official Clips Channel of the Iced Coffee Hour Podcast. All of the Iced Coffee Hour Clips are posted here for your enjoyment! Podcast hosted by Graham Stephan and Jack Selby. Jack Selby: https://www.instagram.com/jlsselby/ Graham Stephan: https://www.instagram.com/gpstephan/